A Surcharge Fee, also called a Checkout Fee, is defined by Visa as “an additional fee that a merchant adds to a consumer’s bill when he or she uses a card for payment.”

Not if you are in one of the following states: California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas.

If you are in one of the other 40 states who do not prohibit surcharges, as of January 27, 2013 you are allowed to; however there are a lot of hoops to jump through first.

All merchants are required to register with Visa and/or MasterCard at least 30 days in advance. You can do this by going to Visa’s website www.visa.com/merchantsurcharging, or MasterCard’s website at www.mastercardmerchant.com. You must also notify your processing acquirer, or the bank which is moving the funds.

Merchants are not allowed to surcharge debit cards or prepaid credit cards. Only Credit Cards may be surcharged, however you must choose exactly how you will do so. You have the option to surcharge at the “Brand Level” or the “Product Level”, but not both.

Simply put, if it has the MasterCard or Visa logo on it, (but not a debit card) you surcharge it. This method is the simplest for your employees to implement. The only thing they need to know is to check if it is a debit or prepaid card.

This method is much more complicated. You can choose to surcharge just certain types of Visa/MasterCards. For example, your store may choose to only impose a surcharge on people who pay using the Visa Signature Card. This makes it much more difficult for your employees to accurately surcharge the customer, as they will need to examine the card at every transaction to determine if it is a Visa Signature card or not.

Note: There is a “Level Playing Field” limitation. Simply put, if you accept all of the major card brands (i.e. Visa, MasterCard, Discover, and American Express), you must also surcharge a similar or more expensive card the same. Also, if a similar card prohibits surcharging, it’s not allowed on the others either. “The amount of the surcharge on the competing payment network brand must equal at least the lesser of: the cost to accept the competing brand’s credit cards or the surcharge imposed on Visa/MasterCard Credit cards.

Finding the Surcharge Rules for American Express and Discover has proven elusive. We have not found published rules for American Express or Discover. They may not allow surcharging, which may mean, you may not be able to surcharge other comparable Visa/MasterCards either.

MasterCard states, "…(if) that competing brand limits the merchant’s ability to surcharge, the merchant may surcharge MasterCard credit cards only in the same way as the merchant would be allowed to surcharge the competing brand’s cards…"

Until the rules are clearly defined, it may be a risk because Visa and MasterCard require that “Level Playing Field” limitation.

The absolute MOST you can surcharge is 4% on a transaction. HOWEVER, Visa states, "The surcharge must not exceed your cost of acceptance for the credit card." The question is, how do you know what that number is? There are over 400 different types of credit card that all have their own costs associated with them. Have you ever looked at your processing statement? It can be extremely confusing! Most merchants pay between 1.5% and 3% on a typical credit card transaction.

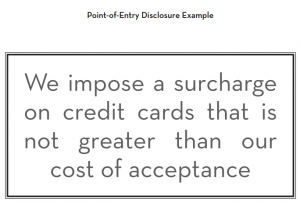

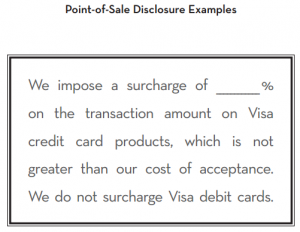

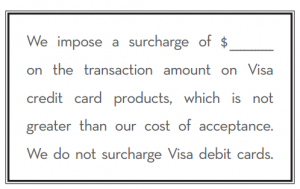

You must disclose to your customers your surcharging policy at the point of entry and the point of sale.

Disclosure at the Point of Entry

Disclosure at the Point of Sale

You are required to disclose the exact dollar amount of the surcharge on each receipt. This must be its own line item on the receipt. Here’s the problem with that, most countertop terminals do not have programming capable of supporting this requirement. At the time of this article, only Point of Sale software is able to add this to the receipts.

In the end, it’s up to each business to decide, unless you live in one of the 10 states prohibiting surcharging. Some questions you should consider prior to your decision:

What will my customers think?

What will my competitors do?

Does my equipment support the programming required to disclose the surcharge on the receipt?

Do I know how much it costs me to accept a credit card?

Can I figure it out?

Is it worth the time, expense, and risk to surcharge my customers for credit card transactions?

Remember, surcharging could make some customers upset enough to walk out of your business and not come back. So far, most large retailers have said they are not planning to impose a surcharge on their customers.

One article we found said:

I think the most likely candidates for this fee are mom and pop stores, where these fees cut too deep into their bottom line. However, the NRF (National Retail Federation) said they don’t even think that will happen because it will be too time-consuming and costly to re-configure their computer system to accommodate the change. Time will tell.

www.visa.com/merchantsurchargingwww.mastercardmerchant.comwww.mastercard.us/merchants/support/surcharge-rules.htmlwww.PaymentCardSettlement.com www.Clearent.com/surcharging

Written by: Katie Gjerde